CBAM in a Nutshell

The Carbon Border Adjustment Mechanism (CBAM) is a strategic EU1 policy that integrates carbon costs into cross-border trade. It is implemented by applying a carbon price to imported goods based on their embedded emissions, thereby mitigating carbon leakage and ensuring competitive parity between EU and non-EU producers. The mechanism sends a strong market signal through mandatory emissions reporting and verification, with carbon pricing methodologies fully aligned to the EU Emissions Trading System (EU ETS).

From a financial perspective, exporters with high carbon intensity face an estimated 15–30% cost uplift on product prices if technological mitigation measures are not implemented ahead of full CBAM enforcement in 2026 (Rabobank, 2025). By aligning carbon pricing and compliance standards with the EU’s domestic carbon market, CBAM ensures imported products carry equivalent emissions liabilities, effectively transforming carbon efficiency into a strategic determinant of international trade competitiveness.

Who Gets Impacted?

CBAM initially applies to EU imported commodities with high produced emissions and carbon leakage risk, including steel, cement, aluminium, fertilizers, hydrogen, and electricity. It covers approximately 113 million tonnes of global export volumes annually (S&P Global, 2025). However, its implications extend well beyond sectoral boundaries, systematically exposing producers with limited access to low-carbon energy and countries characterized by carbon-intensive power grids or weak MRV2 frameworks.

Indonesia is exposed as an exporter of iron and steel and fertilizers to the EU, although its absolute volume relatively low, accounting for only around 9% of total exported iron and steel exports and 1.5% of exported fertilizer globally (Trading Economics, 2024). Indonesia and other impacted developing economies such as India, Brazil, and Vietnam, are also struggle with limited regulatory readiness for low-carbon transitions, directly borne decarbonization costs to companies. This challenge is further compounded by continued reliance on fossil-based power generation, increasing Scope 2 emissions and compliance costs and weakening competitiveness in the EU market.

Meanwhile, competitors such as Türkiye and South Korea have made material progress in establishing robust MRV systems and emissions trading frameworks, allowing carbon costs to be partially internalized domestically and offset against CBAM obligations for EU-bound exports. This regulatory preparedness structurally lowers their effective carbon exposure at the EU border and provides greater pricing flexibility and cost competitiveness in the EU market.

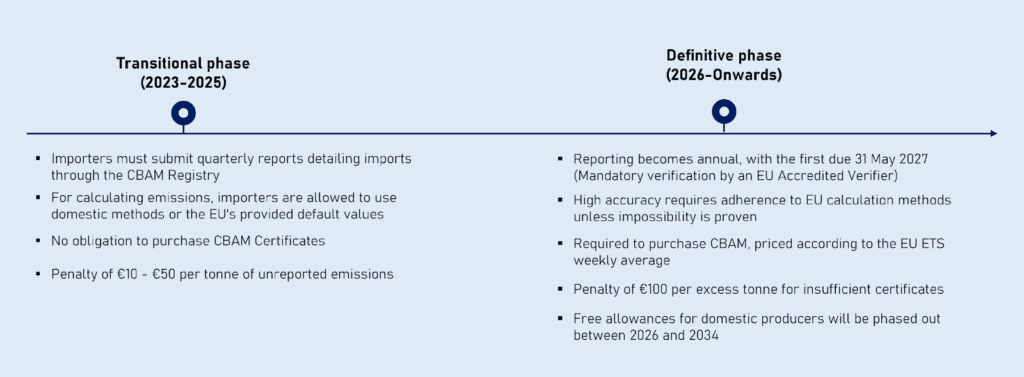

Supply Chain Friction or Decarbonization Accelerator?

As CBAM enters its definitive phase (Figure 1), exporters face a dual compliance challenge. Beyond managing internal emissions, companies are required to trace and verify emissions data across upstream suppliers, materially increasing complexity and execution risk across the supply chain. Where suppliers lack MRV readiness, data discontinuities and verification delays can disrupt customs clearance and, in some cases, constrain access to the EU market.

Figure 1. Timeline of CBAM Implementation

In parallel, EU ETS prices at approximately €90/tCO₂ convert carbon intensity into a visible and unavoidable cost at the EU border, reducing pricing flexibility for exporters embedded in carbon-intensive supply ecosystems. Collectively, these dynamics compress margins and erode competitive positioning relative to peers with cleaner, CBAM-ready value chains.

At the same time, CBAM functions as a structural catalyst for industrial decarbonization rather than a purely compliance-driven mechanism. The transition period provides exporters with a defined window to establish credible emissions baselines while shifting toward renewable energy and advanced abatement solutions. Increased emissions transparency reshapes competitive dynamics by enabling low-carbon product differentiation and improved access to premium markets and greener procurement channels. This direction is reinforced by the EU’s €60 billion commitment under the Global Europe program, exceeding projected CBAM certificate revenues of approximately €9 billion per year and signalling long-term policy durability (European Union, 2021).

As EU ETS prices are expected to rise toward €140/tCO₂e by 2030 (Carbon Trust, 2025), capital allocation will increasingly favour low-carbon systems, leaving only producers with structurally low carbon intensity competitive in future global supply chains.

Strategic Response to Stay Competitive Under CBAM

CBAM elevates decarbonization from a compliance issue to a competitive imperative, demanding alignment across technology, data systems, and capital strategy.

- Implement High-Impact Technology Roadmap

Pivot corporate investment toward a “Net-Zero Industrial Core” by integrating renewables, low-carbon, and carbon capture technologies. This approach leverages low-carbon performance as a competitive advantage, mitigating EU ETS volatility and securing premium market access. - Establish a Digitalized & Audit-Ready MRV System

Deploy a digital, EU-aligned MRV ecosystem to embed carbon accounting into core business operations. High-integrity data ensures the organization avoids punitive default values 3securing a transparent competitive advantage in the global green procurement landscape. - Maximize Strategic Green Financing & Tech Partnerships

Capitalize on international green financing and the EU’s “Global Europe” funds to de-risk technological transitions. Engage in cross-border strategic partnerships to facilitate rapid technology transfer and co-invest in low-carbon materials, ensuring the supply chain remains cost-competitive against global peers.